Australians need good financial advice more than ever to pay for soaring interest rates. Here's how to get it

- Written by Peter Martin, Visiting Fellow, Crawford School of Public Policy, Australian National University

Hundreds of thousands of us who took out fixed-rate mortgages in 2020 and 2021 are about to be hit with massive increases in payments.

After nine successive interest rate increases and at least two more to come, even those of us on variable rates will soon be paying as much as A$1,000 a month more.

With such an uncertain economic outlook, should we switch our super fund’s investment strategies from “growth” to “conservative”? Should we rent rather than buy while home prices fall?

We need answers to our financial questions – but they’re now much harder to get.

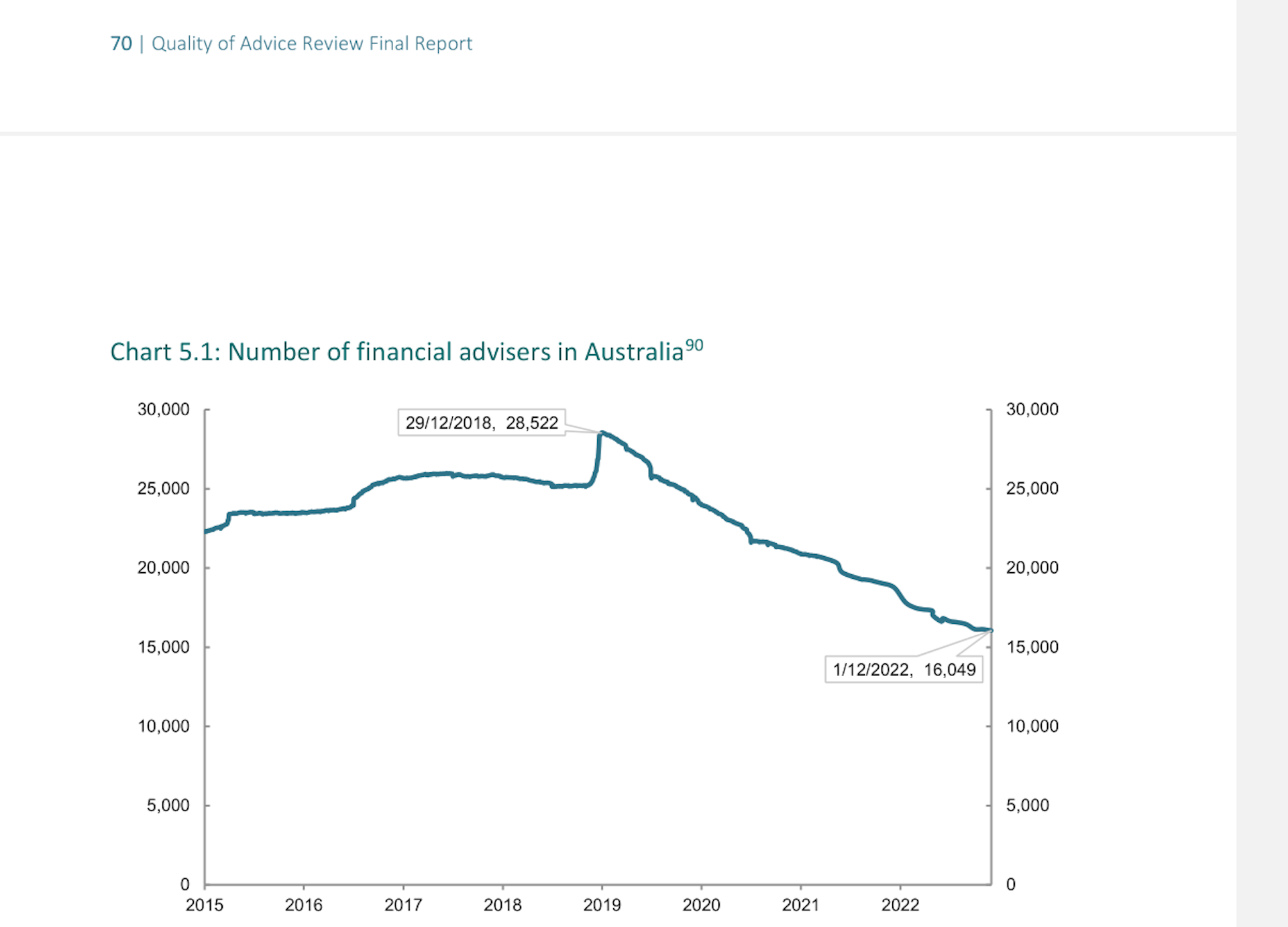

Five years ago, Australia had 28,000 financial advisers. Today there are 16,000. That’s according to a review of financial advice commissioned by the previous government and released by the Albanese government last week.

Thousands of advisers are leaving the industry each year. The ones that remain are charging far more than they used to – $3,710 is said to be common, up 48% in five years, and enough to turn many people away.

So how did it come to this? And what does the new report recommend we do to make it easier for more Australians to get good, more affordable financial help?

Fixing rorts, where even dead people paid a price

This is a story about how Australia, under successive Labor and Coalition governments, let aiming for what’s perfect get in the way of what’s good. Up until I read the Quality of Advice Review last week, I was guilty of doing it too.

For years, I argued we should make financial advice perfect: delivered by genuinely professional advisers, who weren’t receiving kickbacks from firms wanting access to our money. I also argued we should pay for that advice in full upfront, because, whatever the cost, the advice will save us money in the long run.

We needed to do something. Back before a series of explosive Four Corners reports and the 2019 Hayne royal commission into the financial services industry, advisers and the funds they pushed us towards sucked money out of our accounts and presented us with options that made money for them – rather than us.

Read more: Royal commission scandals the result of poor regulation, not literacy

The consequences were shocking. Dead people were being charged for financial advice, and even for life insurance. Gym instructors and other “introducers” were used to lure people into products that charged unnecessarily high fees.

The professionals we now call investment advisers used to be called insurance salesmen. They were paid through commissions to beguile us into signing up for products that charged high fees and paid them high ongoing commissions.

Unintended results of tougher standards

Ahead of the Hayne royal commission, things began to change.

The Rudd Labor government outlawed commissions and introduced legislation requiring advisers to “place clients’ interests ahead of their own”. After winning government, the Coalition tried to undo the changes, before adopting just about the lot after Hayne reported.

It’s now illegal for financial advisers to accept commissions (although mortgage brokers and people who sell insurance still can) and illegal to offer advice that isn’t in the “best interests” of the customer taking almost everything into account. This makes it all but impossible for bank tellers and super funds to offer advice.

So I have been having second thoughts about the arguments I once made for no commissions, best interests, and lots of disclosure documents – especially after reading the Quality of Advice Review. Ironically, its release was largely drowned out by coverage of Australians’ growing financial stress.

{kind=link}